A. No, I don’t mind that the distribution of my estate is public record via the Probate Court. (0 points)

B. Yes, I want to keep how much I have and where it goes between me and my heirs. (1 point)

2. Do you or your spouse have children from a previous marriage?

A. No (0 points)

B. Yes but we view our children as part of one big family (0 points)

C. Yes and it’s important that they are cared for along with my spouse (1 point)

3. Do you have a family member that will require help managing their inheritance upon your passing or that qualifies for government assistance?

A. No (0 points)

B. Yes, I have someone I care about that either needs help managing money or whose government benefits would be compromised by inheriting money from me (1 point)

4. Do you own a lot of assets besides your home, retirement accounts and life insurance?

A. No, that’s pretty much it (0 points)

B. Yes, I/we have a notable amount in brokerage accounts and other savings that won’t pass by beneficiary of law (1 point)

5. Do you or your spouse own a business?

A. No (0 points)

B. Yes, one or both of us has a business that would need to be wound down or passed along upon death (1 point)

6. Do you own property in another state such as a vacation or rental property?

B. Not under current law, but if it changed, I might (1 point)

C. Yes (1 point)

Results

Add up your total points to review what might make the most sense for your situation:

0 points: You will probably be fine with just a Will, which requires you to name an executor and will be processed through the local Probate Court in the county where you live.

1 – 2 points: A Trust probably makes sense for you, although depending on your situation, an Intestate Trust created inside your Will could provide the same benefits of a Living Trust. Consult with an attorney to decide.

2 points or more: Some type of Trust is the best way to ensure that your assets are distributed the way that you wish while also possibly saving on fees, administrative headaches and taxes to your heirs.

5 Myths About 529 College Savings Plans

February 05, 2025

As the school year winds down and the invitations to high school graduations start pouring in, I can’t help but think about the day when my own little girl Rachel—who is finishing up her sophomore year—will be sending out her own invitations. It all seems to be going by so fast but fortunately Susan and I have been preparing for that day by saving in a 529 college savings account.

For some of you moms and dads out there, you too have been using this savings vehicle to help pay for those oncoming college expenses but there are a number of myths floating around out there that could cause confusion when it comes time to using these accounts. Understanding each one will help you and I when it comes time to funding our child’s higher education.

Myth #1: Money in a student’s 529 account will not affect financial aid eligibility

Although 529 assets are included in the calculation for financial aid, the good news is that an account owned by the parent is considered a parental asset so its impact would not be as great as it could have been if it were the child’s asset. That said, some advisors (including yours truly) have suggested allowing non-parents to own the account. While that may prevent the assets from being counted, notice that distributions are treated as untaxed income to the beneficiary. For that reason, we suggest non-parents wait until your child’s junior year to pay for the education with those funds.

Myth #2: A child has legal rights to money in a 529 account

Unlike a custodial account where the child is the rightful owner and has a legal right to control the assets upon reaching the age of majority, a 529 account is the property of the owner, which is typically the parent. Owners have discretion over if and when assets are distributed, may roll over assets from one plan to another, and may change beneficiaries as long as the subsequent beneficiary is related to the original beneficiary.

Myth #3: I am required to use my own state’s 529 plan, and the funds must be used toward a college in my own state

This is a common myth that I often hear in workshops but the simple truth is that you may use a 529 college savings (but not necessarily prepaid) account from any state and your child may attend college in any state and still receive the federal tax benefits. However, some states offer state income tax benefits to residents who use the program from their own state. Even better, residents of many states are eligible for state income tax benefits regardless of which state’s plan they use. Now how’s that for spreading the love?

Myth #4: If my child doesn’t go to college, or I use the money for something else, I’ll get hit with a penalty tax on everything I’ve saved

Obviously, the reason we put money into the 529 account is because we hope to use it to pay for qualified higher education expenses, however, unused 529 funds can be rolled into a Roth IRA.

Myth #5: I will have to pay a penalty tax if my child is awarded a full ride

If your child is fortunate enough to receive a scholarship, you may be eligible to withdraw up to the scholarship amount without penalty. Just remember that if the scholarship is tax-free the amount withdrawn from the account that is attributed to earnings may be taxed as ordinary income.

If you’d like to learn more about using a 529 plan to help save for future college expenses, check out SavingForCollege.com.

How To Find The Right Tax Professional For Your Needs

February 05, 2025

There are lots of reasons to consider outsourcing the preparation of your income taxes to a pro, whether you just don’t want to take the time anymore or you have a more complicated situation such as income sourced from multiple states, income from your side gig or just want to make sure you’re taking advantage of any and all tax savings opportunities. It’s important to know that all tax preparers are not the same – there are different credentials and specialties within the world of tax preparation.

The first step in finding a pro is determining what type of preparer you need. Here are the 5 categories to choose from.

The type of preparer you need depends on your situation

Paid tax preparer:

For a routine return (aka you’re married with kids, own a home and have donations and maybe some investment income, but nothing more complicated), a tax preparer from a storefront service like H&R Block or Jackson Hewitt could do the trick. The convenience of extended hours and immediate tax preparation along with the relatively low cost (starting at about $100 on up, depending on the complexity of your return) is what attracts most customers. While most paid tax preparers must pass employer-administered examinations, they may not be as rigorous as those required to gain the designations or certifications other pros hold.

Also keep in mind that anyone can call themselves a tax preparer as long as they have an IRS issued preparer tax identification number (PTIN), but that doesn’t necessarily mean they know what they’re doing. If you’re looking to hire a tax preparer that doesn’t work for a large service, be sure to ask about experience and other credentials. And beware of any preparer asking you to sign a blank tax return or promising you any type of refund guarantee before looking at your information – they’re most likely up to no good and you’re always on the hook for taxes you owe, no matter who prepares your return.

Accountant:

Someone who practices accounting but hasn’t taken or passed the CPA examination may not be a bad choice for a basic return. Seek someone with a personal tax emphasis. Rates can range from $40 to $75 or more per hour.

Enrolled Agent:

EAs are the only taxpayer representatives who receive their right to practice from the United States government. (CPAs and attorneys are licensed by the states.) Agents have either worked for the IRS for five continuous years or have passed a two-day exam, and must complete 72 hours of continuing education every 3 years. Billing may be hourly (usually $100 to $200 per hour) or by the tax return, which can run from $100 (for a basic 1040) on up depending on the complexity. You may choose to work with an EA if you have an unusual tax situation or have past tax issues that you need help cleaning up.

Certified Public Accountant:

A CPA earns the title by passing the Uniform CPA examination, a rigorous 4-part test that ensures those holding the license are knowledgeable in all areas of accounting. CPAs must also complete a certain amount of on-the-job training in auditing and taxes (the amount varies by state) before they can earn their license and then must maintain their license with a certain amount of continuing education each year (varies by state ). Some CPAs specialize in corporate work and may not be the best choice for personal taxes, while others specialize in tax, but not in individual income taxes. A CPA may be the best choice if you have business income, own rental property or have other tax complexities that extend beyond income you earned from working and/or investing.

Tax Attorney:

If your tax situation is very complex or you are in deep trouble with the IRS, you may want to consider a tax attorney. Of course, a tax attorney is the most expensive of the tax pros, with rates typically running from $150 to $600 an hour.

How to find the best one for you

The best place to start your search for a tax pro is with friends and colleagues or even your local chamber of commerce. You can also check with the National Association of Tax Professionals, which has listings with certifications noted. The Better Business Bureau or the pros certifying agency can tell you if the person you’re considering hiring is in good standing, with no disciplinary actions.

Interviewing a preparer before you hand over your W-2 can prevent problems later. Make sure you’re comfortable with their answers to these questions.

What’s your education and experience? (at minimum they should have a college degree or several years of experience with references available)

Are you licensed or registered? By what agency? For how long? (If they are not licensed or registered, ask to talk with other clients to make sure they know what they’re doing)

What’s your specialty (personal taxes, corporate taxes, audit issues)?

What continuing education courses have you taken recently?

Who from your office would work on my taxes? (many larger offices have interns prepare returns that are then reviewed by more experienced CPAs – if that’s the case, you may be better off going to a smaller office and paying less)

In the event I’m audited, could you represent me?

What are your rates, and how much do you expect the total cost of the return to be? (beware of anyone wanting to charge by the form – you could be overcharged. The best preparers either charge by the hour or are willing to give you a not-to-exceed estimate)

When would the return be finished? (if you’re coming to them after mid-March, don’t be surprised if the answer is after the filing deadline – busy tax preparers often file extensions for clients who procrastinate getting their information in on time, although that doesn’t extend your time to pay any taxes due)

Whatever your needs, there’s a tax pro out there ready to make your life easier. Choose the right one, and you’ll more than likely get your money’s worth.

Be A Tax Savvy Investor

February 05, 2025

Take advantage of long-term capital gains rates

Hold stocks and mutual funds for more than twelve months to have your gains taxed at lower capital gains rates.

Consider tax-advantaged investments

Municipal bonds are issued by state and local government agencies. The interest is tax free at the federal level, but may be subject to the alternative minimum tax. Those issued by the state or municipality where you live are tax free at the state or local level as well.

Sell investments at a loss

If you have stocks or mutual funds in a taxable account that are worth less than you paid for them, and your losses exceed your gains, you can take losses of up to $3,000 against your taxable income. Be sure to evaluate selling costs and the investment’s future potential first.

Watch out for the wash sale

You can sell mutual fund or stock losers and buy them back again if you feel they are good long-term investments (but make sure you wait at least 31 days before you buy them back or the IRS will disallow your loss).

Don’t buy mutual funds at the end of the year

Mutual funds may pay out capital gains accrued throughout the year as a taxable distribution toward the end of the year (even if you just bought the fund, you’ll owe taxes on this payout!). Wait until after the distribution is made if you wish to minimize your tax bill.

Know the limit if you’re selling your home

Qualifying homeowners are exempt from the first $250,000 of capital gains ($500,000 if married filing jointly) when they sell their home.

Understand the different tax rates for dividends versus interest

Qualified dividends paid from stock investments are taxed at the same rate as long-term capital gains. Interest earned on investments such as CDs, savings accounts, and money market funds, however, are taxed at higher ordinary income tax rates.

5 Estate Planning Steps Literally Everyone Needs To Take

February 05, 2025

You may be thinking that you do not have the need for an estate plan or at least there is no harm in delaying getting started with estate planning. The truth is that anyone with savings, debt, a spouse, children, a home, or a retirement plan needs to at least have the basics in place.

Hopefully, it’s true that you won’t need it for decades to come, but should something happen and you don’t have a plan, it could make a HUGE difference, sometimes even while you’re still alive.

Here are the 5 critical steps – make a plan to check these off the list today.

Step 1: Create or review your will

If you have a current will, congratulations! You have already taken an important step in the estate planning process. Your will controls the distribution of everything you own that doesn’t have a beneficiary designation and can also name a guardian for any minor children. Things that you pass via will include:

Tangible personal property like your home, your car, and all your stuff

Individually held financial accounts such as savings, checking, stocks, bonds, and mutual funds held outside retirement accounts which do not have a beneficiary designation.

Don’t have a will? If you die without a will, your state has laws that determine who gets your money called laws of intestacy. These laws vary from state to state but generally give first priority to your spouse and children. If you have neither, then blood relatives including parents, siblings, and others are your default heirs, under a specified order of priority. If no blood relatives can be found, your money goes to the state Treasury.

Protect your children! Should your minor children lose both parents, your will determines who will raise them and manage your money on their behalf until they reach the age of majority. If you die without a will, the state will name a guardian to take the children – and it may not be who you think is the most appropriate person!

In your will, you can designate a guardian for your children, as well as one or more alternates in the event your first choice is not available. You can name the same person, or a different one, to manage any money left to your children as well.

Step 2: Review your assets and update beneficiary designations

Many people think that once they have made a will, all of their assets will pass according to that document. Actually, a large number of your most valuable assets are not subject to probate, meaning they may NOT pass by will. Use this checklist to keep track of specific exceptions to your will.

Do you…

Own any bank accounts, mutual funds, or brokerage accounts in joint name with someone else?

-If yes, the joint account owner will automatically own the assets upon your death (in most cases). Also, in most states, you can designate an individual account to be “Payable On Death” (POD) or “Transfer On Death”(TOD) to a named beneficiary for the same result and the account will “skip” your will (and probate).

Own real estate with another person?

-If yes, real estate owned as joint ownership with rights of survivorship also does not pass by your will but goes directly to the other joint owner automatically.

Have insurance policies, annuity contracts, employer retirement plans and/or IRA’s?

-If yes, keep your beneficiaries updated. All of these account types require you to name who will receive the account or policy value upon your death. If you fail to name a beneficiary or all beneficiaries have died before you, the account will be payable to your estate.

Have a trust?

-If yes, your trust will determine how the trust property is distributed to beneficiaries, but only if you take the necessary steps to re-title accounts and other assets to the trust. Failure to change the title to the name of your trust will cause them to pass by other means, regardless of what the trust says.

All of these exceptions pass directly to the person named, and not by your will. It is extremely important to keep your beneficiary designations up to date – it is not uncommon for older life insurance policies and previous employer retirement plans to be paid out to ex-spouses or other unintentional parties. Updating your will does not fix these accounts, since they are not subject to your will.

Step 3: Evaluate your insurance coverage

Whether your income stops due to death or disability, the effect on your family is the same. Where will the money come from to replace your paycheck? Insurance may be your best option. Without it, your family may need to sell assets, move to a less expensive home and/or disrupt college and retirement plans.

Life insurance. Use this calculator to get an idea of how much insurance you need to have in place. Once you decide on the right amount for you, be sure to find out what benefits you have through work first. Sometimes, you can get all of the life insurance you need there at the most affordable rates, but if you can’t, look into supplementing with a personal policy.

Disability insurance. This is your paycheck insurance – should something happen that keeps you from being able to work, this insurance kicks in to replace some of that until you’re able to work again. Statistically speaking, this is the insurance you’re more likely to use during your working years. First, confirm any coverage you have through work and find out if you can add to it, if necessary — most group plans are broken into Short-Term and Long-Term and often have lower premiums than individual policies. It’s important to know that most policies only provide 60 – 70% replacement income, so should you become disabled, you’ll still have a drop in income. Use this calculator to see if you need to purchase coverage beyond what you have through work.

Step 4: Check your powers of attorney

Remember that your will doesn’t take effect until you actually pass away, but what happens if you have an accident or are otherwise unable to make financial or healthcare decisions for yourself? You can designate someone else to make these decisions for you using the following important documents:

Advanced Directives – There are two types of documents, called advance directives, that can be prepared as part of your estate planning for future medical decisions.

Living Wills – If you have strong feelings about what type of medical care you want (or don’t want!) and you are unable to communicate, a living will can do it for you. This is a document that you can use to state under what circumstances you wish to be kept alive by artificial means. If you do not express your views in writing, all available means of treatment to maintain your life are usually provided, even if family members object. Therefore, if there are conditions where you would not want treatment, it is important that you state your wishes while you are able to do so.

Medical Power of Attorney – While the title and wording of this document may vary from state to state, most states permit a document that enables you to select someone to make medical decisions on your behalf. This power can only be exercised when you are unable to communicate but is not limited to situations where you are terminally ill.

Durable Power of Attorney – There can be a number of situations where you may need someone else to make financial transactions on your behalf. Whether you’re traveling overseas, in a coma, or sequestered in a jury, a document called a durable power of attorney permits the person named as your agent to sign documents, trade securities, and sell property. You do not have to be unable to act for yourself in order for your agent to act on your behalf.

The agent does have to act in good faith, and may not abuse the power of attorney for his/her own advantage. If you sign a power of attorney that is not specifically durable, the power is revoked upon your disability or inability to communicate. With a durable power of attorney, your agent can make the necessary transactions in order to pay your medical bills or make sure your family has the money they need.

Living Trust – Another method is to place your assets in a living trust. Don’t confuse this with the living will described above. Although they sound similar, they are very different. A trust is simply an arrangement that provides for a third party to manage your assets for a beneficiary, upon your death. A living trust allows you to start a similar arrangement while you are still alive. You can be your own trustee, and simply name a successor trustee to take over upon your death or disability. A living trust is a more expensive estate planning tool than a durable power of attorney, but it can also be customized to your specific needs. It is particularly useful for more complicated situations such as second families or people who own property in multiple states.

Step 5: Monitor your estate plan

Things change. That’s why you should review your estate plan whenever a life event occurs for you and your family. Even if it seems like nothing’s changed, you should review your estate plan every few years at a minimum. A good rule of thumb is that you should update your will any time someone enters or leaves your life (aka birth, marriage, divorce, death)

Documents to review

Your will and any trusts

Powers of attorney

Beneficiary designations on employer-sponsored retirement plans (401(k), 403(b), 457, etc), IRAs, life insurance policies, annuities, HSAs

An estate plan, like a financial plan, is always evolving as your life changes. It can be easy to delay making an estate plan because there are several important decisions you must make, but don’t fall victim to analysis paralysis. You can always change your documents as long as you’re still of sound mind, so choose what works for your life today, and then make updates as things change. Also, be sure to check with legal benefits offered by your employer to help with the estate planning process.

How to Invest in a Taxable Account

February 05, 2025

Investing in your retirement account can be quite different from investing in a taxable account. Here are some options to consider when investing in a taxable account:

Use it for short term goals. One of the advantages of a taxable account is that you don’t need to worry about any tax penalties on withdrawals. For that reason, it probably makes the most sense to use a taxable account for goals other than retirement and education like an emergency fund, a vacation, or a down payment on a car or home. In that case, you don’t want to take risk so cash is king. To maximize the interest you earn, you can search for high-yielding rewards checking accounts, online savings accounts, and CDs on sites like Deposit Accounts and Bankrate.

Keep it simple for retirement. Just like in a 401(k) or IRA, you can simplify your retirement investing as much as possible with a target date fund that’s fully diversified and automatically becomes more conservative as you get closer to the target retirement date. There are a couple of differences in a taxable account though. The bad news is that you’ll be paying taxes on it each year so you want a fund that doesn’t trade as often. The good news is that you’re not limited to the options in an employer’s plan so you can choose target date funds with low turnover (how often the fund trades and hence generates taxes) like ones composed of passive index funds.

Invest more conservatively for early retirement. If you plan to retire early, a taxable account can be used for income until you’re no longer subject to penalties in your other retirement accounts or to generate less taxable income so you can qualify for bigger subsidies if you plan to purchase health insurance through the Affordable Care Act before qualifying for Medicare at age 65. In either case, you’ll want to invest more conservatively than with your other investments since this money will be used first and possibly depleted over a relatively short period of time. Consider a conservative balanced fund or make your own conservative mix using US savings bonds (which are tax-deferred and don’t fluctuate in value like other bonds do) or tax-free municipal bonds instead of taxable bonds if you’re in a high tax bracket.

Make your overall retirement portfolio more tax-efficient. You can also use a taxable account to complement your other retirement accounts by holding those investments that are most tax-efficient, meaning they lose the least percentage of earnings to taxes. Your best bets here are stocks and stock funds since the gains are taxed at a capital gains rate that’s lower than your ordinary income tax rate as long as you hold them for more than a year. In addition, the volatility of stocks can also be your friend since you can use losses to offset other taxes (as long as you don’t repurchase the same or an identical investment 30 days before or after you sell it). When you pass away, there’s also no tax on the stocks’ gain over your lifetime when your heirs sell them.

In particular, consider individual stocks (which give you the most control over taxes) and stock funds with low turnover like index funds and tax-managed funds. Foreign stocks and funds in taxable accounts are also eligible for a foreign tax credit for any taxes paid to foreign governments. That’s not available when they’re in tax-sheltered accounts so you may want to prioritize them in taxable accounts over US stocks.

For retirement, you’ll probably want to max out any tax-advantaged accounts you’re eligible for first. But if you’re fortunate enough to still have extra savings, there are ways to make the best use of a taxable account. Like all financial decisions, it all depends on your individual situation and goals.

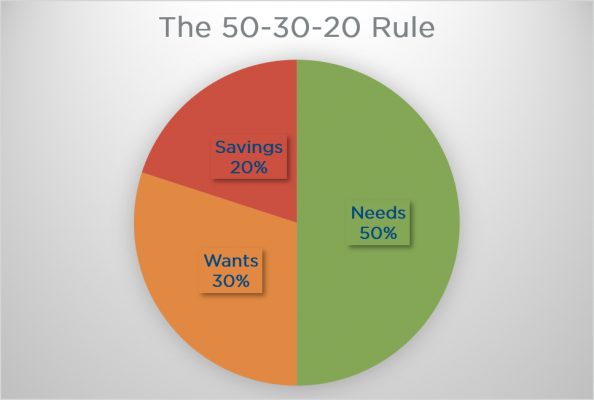

Financial Rules of Thumb: The 50-30-20 Rule

February 05, 2025

One way to measure whether or not a particular expense or goal fits into your spending plan is to measure it against your existing financial goals and commitments. A popular way to look at this is called “The 50-30-20 Rule.”

The 50-30-20 Rule

The rule basically says that one way to achieve financial security is to limit your fixed expenses (or needs) to 50% of your after-tax income, your discretionary expenses to 30%, and setting aside 20% toward your goals. Let’s break that down by type so you can see what we mean.

50% to “needs.”

Examples of things that fit in this category include:

Housing

Transportation

Food

Clothing

Utilities

Healthcare

One part of this rule that’s often debated is how much of these categories are true needs versus wants (or discretionary spending). Let’s take the purchase of a vehicle as an example. How much you spend on a vehicle can vary widely. For many people, having a vehicle is a need. They need it to get to work and earn money to pay bills. On the other hand, plenty of people live in big cities who get by just fine without this “need!” Likewise, we all need food to live and clothing to avoid being arrested in public. However, spending on these two categories very easily bleeds over to wants.

Making trade-offs

So you have to be honest with yourself about whether the things you’re putting in this category are absolutely vital to your life or if part of the expense could be classified as a want. Maybe another way to think of it is as a trade-off — it’s fine to spend more on housing if having a more expensive place is important to you; it just means you’ll need to spend less on a car to make it balance.

30% to “wants.”

Examples here include:

Entertainment, including cable

Dining out

Gym membership

Hobbies

Personal care beyond the basics

Cell phone beyond the basic plan

As you can see, the rules can be tricky, so you have to be honest with yourself. Most of us need regular haircuts to maintain a decent appearance. However, spending on a pricey salon cut goes above and beyond, so it belongs in this category.

20% to goals

This category obviously includes savings (including what you put into your retirement account at work) and includes debt payments. So if you’re paying $250 per month on a student loan, that counts toward your 20%.

Tying it all together

Remember, this rule is meant to be a guideline, particularly when you’re just getting started and have no idea what you should be spending on things like rent or a car payment. But it can also offer insights into areas where you may need to cut back. For example, if you run your own numbers and find that your needs far exceed 50%, it may be time to think bigger picture about making some changes – do you need to sell your car for a cheaper payment? Think about moving to lower housing or transportation expenses?

This rule can help show you whether or not you can afford to add a new want into your life. If your wants are way beyond 30%, that definitely means that you can’t afford to add a payment for something like a boutique fitness membership, cleaning service, or upgraded cable package to your life at this point.

What To Do If Brokerage Firms Don’t Report Wash Sales for RSUs

February 05, 2025

The amount of data that flows through the services of large record-keeping institutions is mind-blowing. But, as much as we rely on them for accuracy in reporting, we also need to record and monitor our own cost basis for tax purposes.

Restricted Stock Units (RSUs) are a popular form of employee (stock) compensation many companies use. RSUs allow employees to earn stock in their company over time, often as a reward for meeting performance targets. However, when it comes time to report these RSU awards on tax returns, combined with the subsequent purchases and sales of the company or other stock, many employees can be confused and frustrated with broker reporting. Careful planning can help maximize your return and prevent costly mistakes.

Cost basis is the original price for a given security, whether purchased or vested. The cost basis of stock from an RSU is typically the fair market value at the time of vesting. When the stock (received after vesting of RSUs) is ultimately sold or transferred, either in part or in full, the cost basis is used to determine the taxable gain or loss on the transaction.

A wash sale occurs when you sell or trade stock or securities at a loss, and within 30 days before or after that sale you:

Buy, or vest in, substantially identical stock or securities (SISS),

Acquire SISS or securities in a fully taxable trade,

Acquire a contract or option to buy SISS, or

Acquire SISS for your IRA, Roth IRA, SEP, or Simple,

Sell stock, and your spouse or a corporation you control buys a substantially identical position.

Note: Vesting in RSUs is considered an acquisition for wash sale purposes. If you sell shares within 30 days of vesting, you may not be allowed to deduct your loss on the sale (see Example 2 from the Wash Sales section of IRS Publication 550).

If your loss was disallowed because of the wash sale rule, all is not lost! You would add the disallowed loss to the cost of the new stock or securities (although this would not be meaningful in an IRA because IRAs are not subject to capital gain tax treatment). The result is an increase to your basis in the new stock or securities. This adjustment postpones the loss deduction until the new stock or securities are sold. Your holding period for the new stock or securities includes the holding period of the stock or securities sold (long-term vs. short-term).

Unfortunately, firms are not required to add disallowed losses to the cost basis of equity compensation, such as RSUs, when a wash sale occurs. This lack of reporting makes it difficult for employees to accurately report these types of sales on their taxes. In the absence of wash sale reporting, employees should take steps to keep accurate records of their RSU/stock activities. This includes recording the grant date, the fair market value at the time of vesting, and any subsequent sales or transfers of the stock from RSUs or purchase of the same stock outside of the employee’s RSU benefit. If the stock generates dividends, those will also need to be recorded. By maintaining these records, you’ll have the information you need to report activity on your tax returns accurately.

Firms are also not required to calculate wash sales on options trading. This places an additional burden on the taxpayer when it comes to accurately reporting sales activity on tax returns.

Lastly, suppose you hold the same stock or a substantially similar investment (like a mutual fund or ETF) through other brokerage firms, and a wash sale is triggered. In all wash sale cases, you are responsible for calculating and reporting this information when filing tax returns. You would gather all your account activity and 1099-B forms from multiple brokerages and use Form 8949 to report buy/sale information for your taxes.

The lack of reporting by firms for RSUs has created a significant burden for employees and tax professionals. Until more comprehensive reporting requirements are implemented, employees should take the necessary steps to keep accurate records of RSU activities to avoid any tax issues. Consult with a tax professional if you have any questions or are unsure how to proceed, especially if you live or work in multiple states and countries. By making informed decisions, you can maximize your returns and minimize your taxes regarding RSU investments.

Working In the U.S. Temporarily? Here’s What You Need to Know About Retirement

February 05, 2025

We get many retirement benefits questions on our financial coaching line from professionals working in the United States but plan to return eventually to their home countries or take another ex-pat assignment. Frequent questions include: should I participate in my company’s 401(k) plan, and if so, should I choose to make a pre-tax, Roth, or after-tax voluntary contribution? In addition, how can I access my savings when I leave the US?

Get professional tax advice

If you’re a professional from another country working legally in the United States and do not have permanent resident status (e.g., a “green card”), the US taxation system can seem like a maze: one wrong move, and you’re stuck in a corner. Do not try and navigate this yourself. Instead, seek professional tax advice from a tax preparer experienced in ex-pat/non-citizen issues. You’ll need guidance on federal and state withholding, tax treaties, tax filing, benefits choices, and what to do when you leave the US.

Ask ex-pat colleagues first for referrals to a tax professional with experience working with people like you. It’s not expensive and could save you from financial and legal problems later. For a basic overview of types of US tax preparers, see How to Find a Good Tax Preparer.

What do I need to know about US retirement savings programs?

This is the government-sponsored retirement system, similar to what’s often called a “public pension” in other countries. As a non-citizen employee, you will likely pay the same taxes as US citizens into Social Security and Medicare, which you will not recoup unless you continue to be a US resident. Your employer will also make contributions on your behalf.

If you do not plan to live in the US when you retire, you may or may not be able to receive Social Security income benefits. It depends on how long you paid into the system, your immigration status, country of residence, and whether you started receiving payments before leaving the US.

401(k), 403(b), and 457 plans

Most large employers offer employer-sponsored retirement savings plans, such as 401(k) and 403(b) plans. Employees may contribute a percentage of their gross pay each period to a tax-advantaged account. Frequently, the employer will match up to a set percentage of what you contribute or will sometimes make contributions regardless of whether you make your own contributions.

In addition, you’ll get to choose how your contributions are invested from a menu of mutual funds or other investment vehicles. You may also choose whether you contribute your money into a pre-tax (traditional), after-tax (Roth), or after-tax voluntary account. See tips below for determining what works for you.

IRA and Roth IRA

If you are considered a resident for US tax purposes (have US earned income, have a Social Security number, and meet the substantial presence test), you may open a traditional or Roth IRA. However, if you are a non-citizen and don’t plan to seek US citizenship or permanent residency, you may not be able to reap all the benefits of an IRA or Roth. If you’re eligible, you may contribute up to certain limits.

IRA limit

IRA catch-up amount

401(k)/403(b) limit

401(k)/403(b) catch-up amount

SIMPLE limit

SIMPLE catch-up amount

SEP

2025

$7,000

$1,000

$23,500

$7,500

$16,500

$3,500

$70,000

2024

$7,000

$1,000

$23,000

$7,500

$16,000

$3,500

$69,000

Traditional pension plans

These are no longer widely available to new employees, but some larger companies and state/local government jobs still offer them. A pension may be fully funded by employer contributions or by combining employer and employee contributions. Typically, it takes 10-20 years to be “vested” in a pension, where the employee is eligible to receive a fixed monthly payout at retirement.

Should I enroll in my 401(k)?

Saving in your employer-sponsored retirement plan has multiple benefits, even if you don’t plan to continue working and living in the US later in your career. If there’s a match on your contributions, that’s like earning additional income. There’s the potential for tax-deferred or tax-free growth, depending on the type of contributions you make. Plus, you can’t beat the ease of contributions deducted automatically from your paycheck!

Always consider your future taxes.

For non-citizens making decisions about which retirement contribution type to choose, you’ll need to consider where you will be living when you withdraw the money, how old you will be when you plan to withdraw it, and whether you think you’ll be a US permanent resident or citizen at that time. If you still expect to be a non-citizen when you withdraw the money, note that you must file a US tax return in any year in which you have US income, including retirement plan withdrawals. According to the IRS, “Most U.S.-source income paid to a foreign person are subject to a withholding tax of 30%, although a reduced rate or exemption may apply if stipulated in the applicable tax treaty. You may or may not owe that rate in taxes, but the funds will be withheld from the distribution regardless.

If you’ve overpaid through the withholding, you will get a refund after filing your tax return for that year. See this IRS US Tax Guide for Aliens for in-depth reading. Now, do you see why I say you need a tax advisor if you’re an ex-pat working in the US?

If by the time you withdraw the money, you have become a US citizen or a permanent resident but are living overseas, you won’t be subject to the 30 percent withholding. You will, however, have to file a US income tax return every year regardless of your income.

For U.S. citizens, check out this article about what you need to know about taxes while working and living abroad.

Pre-tax, Roth, or After-tax voluntary contributions?

The financial planning goal is to minimize taxes and penalties. Your company’s matching or profit-sharing contributions to your retirement plan are always pre-tax, so they will be taxed when you withdraw them. How much of your retirement contributions will be taxed depends on how you contribute:

Traditional pre-tax contributions are deducted from your taxable income, so you’ll pay less in income taxes today. Earnings grow tax-deferred for retirement. After age 59 1/2, you may withdraw them without penalty, paying US income taxes on whatever you take out. Before that, you may withdraw them only if you a) retire, b) leave the firm, or c) have an extreme financial hardship.

Roth contributions: Roth 401(k) contributions are made after-tax and grow tax-free for retirement if withdrawn 1) after 5 years and 2) after age 59 ½. Therefore, if you meet those requirements for distribution, your Roth distribution would not be included in your taxable US income. See this IRS tool to see if your Roth distribution could be taxable. However, your home country (or country of residence) could tax it, depending on the tax treaty with the US.

If your plan allows, you can leave the funds in the account until after age 59 ½. If you must take an earlier distribution after leaving the firm, you will only be taxed and penalized on the related growth and company contributions, not your original contributions. See this IRS Guide to Roth 401(k)s for more information.

After-tax voluntary contributions: Many employer-sponsored plans permit after-tax voluntary contributions above, or as a substitute for, Roth or pre-tax contributions. This will give you some flexibility, as you may withdraw those contributions at any time (although the growth of your funds will be subject to tax). If you plan to withdraw contributions after leaving the firm, taxation is similar to the Roth 401(k). Your retirement plan may also permit you to convert after-tax voluntary contributions to the Roth account, which could come in handy if you end up staying in the US, or roll them over to a combination of a traditional IRA and Roth IRA when you leave the firm.

On the downside, you typically won’t receive an employer match on voluntary contributions. Your original contributions can be withdrawn at any time tax-free, but any earnings or growth made in the account will be taxed when withdrawn. (That means gains withdrawn before 59 ½ will be taxed and subject to an additional 10 percent penalty.)

If you leave the US, are you required to take distributions?

If you leave to work and reside overseas, you would be able to take a distribution from your company’s retirement plan but are generally not obliged to take any until age 73. If possible, leave it to continue to grow, protected from taxes. Pre-tax contributions later distributed are included in your taxable income and, if taken before age 59 1/2, may be subject to an additional 10% penalty.

Ask for guidance

If your company offers a workplace financial wellness benefit, talk through the pros and cons of your choices with a financial coach. Your financial coach can help you understand the implications of your options, given your personal situation. Also, while you’re working in the US, don’t forget to use a tax advisor experienced in non-resident taxation., such as a certified public accountant or an enrolled agent. This is well worth the relatively low cost of getting good tax advice.

Is It Ever OK To Borrow From Your 401K?

February 05, 2025

Ideally, never…or at least rarely. Plundering our retirement piggy banks can be tempting when a financial emergency arises or perhaps when we are looking for cash to finance a home purchase or to pay off some high interest credit cards.

Although IRS rules do allow for retirement plan loans, the maximum loan size is either (1) the greater of $10,000 or half of your vested 401(k) balance or (2) $50,000, whichever is smaller. While borrowing from yourself in this way can be convenient and seem relatively harmless, this type of short-term fix may have some long-term consequences that are more expensive than we realize.

401(k) loans seem attractive…at first. On the one hand, borrowing from our company retirement plans is tempting for several reasons:

No credit check is required and consequently, it will not affect your credit score.

The interest rate is potentially lower than that of a traditional loan.

You pay back the loan conveniently through payroll deduction.

You are borrowing your own money and paying yourself back with interest. Where’s the harm, right?

Then things can get ugly. A closer examination of exactly how all of the moving parts work as well as some of the things that could potentially go wrong might lead you to conclude that getting a bank loan, borrowing against home equity, selling other assets, or even borrowing from family might be better for you in the long run. Here are some of the reasons to think twice before taking out a 401(k) loan:

You will pay taxes on the same money twice. It is true that you pay yourself back with some interest, but you also use after tax dollars to make those interest payments. In the future, when you spend your pre-tax 401(k) money in retirement, those future interest distributions will be taxable as ordinary income, meaning you actually pay taxes twice on that money.

Lost growth and compounding. The money you borrow from your 401(k) is temporarily removed from the underlying investments, missing out on any market growth, interest, dividends, etc. The double whammy comes from the missed opportunity for this growth to be reinvested and earn even more through compounding, which is the financial superpower that comes from investing – and staying invested – over time.

Treating your 401(k) like an ATM. Once you dip into your retirement stash and use it to relieve some type of financial pain, you can begin to slide down a slippery financial behavior slope. Having rewarded yourself once with a relatively easy source of cash, you run the risk of training your brain to think of this strategy as a reasonable substitute for creating and maintaining better financial habits, such as regularly saving cash in an emergency fund, sticking with a budget, or increasing your retirement plan contribution rate. Staying faithful to healthier financial priorities helps you avoid disturbing your retirement plan’s progress by treating it like an automated teller machine and dipping into it multiple times.

Less take-home pay. While you are repaying your loan, your paycheck will be reduced by the amount of the loan repayment. If your cash flow was tight before raiding your retirement fund, you may soon discover that it becomes even more challenging with a reduced paycheck.

Severe taxes and penalties. If you leave your employer for any reason – whether it is your idea or if your employer fires you – you might have to repay the entire remaining loan balance within as little as 60 to 90 days. This requirement varies from plan to plan. Some company retirement plans allow you to continue making the scheduled loan repayments without having to pay it all back early.

However, your payments obviously will no longer come from payroll deduction once your job ends. If your period of unemployment is lengthy, you might not be able to keep up with the required repayment schedule.

Once you default on a 401(k) loan, the IRS then treats any remaining balance as a taxable distribution. If you are under age 59 ½ at that time, there may be an additional 10% tax penalty for taking an early withdrawal from your retirement plan. What was once a temporary financial fix could quickly become an expensive tax bomb.

It might be okay to borrow once, if:

You have high interest rate (think double-digit) debt and you have exhausted all other opportunities to refinance or negotiate a lower interest rate. The ongoing challenge will be to reduce any temptation to begin using the same high interest credit cards or loan sources again and recreate the problem. Once you pay back the 401(k) loan, take that monthly loan payment you were making and redirect it to a savings account at your bank, building up an emergency fund you can use for future financial emergencies, rather than raiding your retirement plan like a pirate.

You owe the IRS back taxes. With interest and penalties stacking up on overdue taxes, this financial burden can become very serious over time. In this case, a 401(k) loan might be your saving grace. However, you may qualify for relief under the IRS guidelines for alternate payment plans and hardship.

You are in real danger of defaulting on a student loan. In most cases, bankruptcy is not an option for these.

You are facing imminent bankruptcy or eviction from your home. Talk to a nonprofit consumer credit counselor (nfcc.org) about alternatives to bankruptcy. If a 401(k) loan can buy you some valuable time while you restructure your cash flow and other investments to support a sustainable strategy and repay your 401(k) loan, this might be an appropriate financial move.

The important thing to keep in mind regarding loans from your retirement plan is to make sure you address the underlying need for cash rather than simply assuming the 401(k) loan will solve the immediate problem. Otherwise, you could find yourself on an unhealthy financial treadmill where you repeatedly borrow from your 401(k) and begin to seriously jeopardize your ability to retire on time, comfortably, or both.

A good way to see just how damaging and expensive a retirement plan loan can be to your financial future is to use a 401(k) Borrowing Calculator. This calculator shows how much less money you may have for retirement if you borrow from your retirement plan versus not taking out a 401(k) loan.

Bottom line: make sure you have carefully considered all other alternatives before you undo much of the hard work you have already invested in growing your retirement nest egg.

This post was originally published on Forbes.com, August 3rd, 2017.

Why You Need to Start Saving Money RIGHT NOW

February 05, 2025

Pretty much every personal finance resource will tell you that the earlier you start saving, the better off you’ll be due to the effect of compound interest. It’s a bit of a, “well, duh,” thing, but there’s more to it than just the fact that you’ll have longer to save if you start early. The thing is, the earlier you start, the earlier you can actually stop saving if you want to. Continue reading “Why You Need to Start Saving Money RIGHT NOW”

Here’s Why You Need to Stop Measuring Your Financial Progress Against Your Income

February 05, 2025

Did you find yourself looking at the total income amount on your tax return for last year and thinking to yourself, “Well, I certainly don’t FEEL like I make that amount of money?” You’re not alone. One of the most self-destructive financial beliefs that I see as a financial planner is people justifying living outside their means because they have the idea that someone who makes what they do should be able to have the things that they want. Here’s the thing: they were already living like they made this amount of money before they got there.

They find themselves in debt because they just couldn’t wait to have the new house with the furniture and that amazing vacation to Italy. Then they had kids who now have all the gadgets (and of course, they need a comfortable, stylish car to drive them around in). Sound familiar? Welcome to the club!

So now that they’re here, stuck paying off the stuff they bought when they borrowed against this higher income they knew they’d eventually make, they find themselves struggling to prioritize paying off that debt versus saving for college, a bigger home for their growing family and retirement. And as they struggle, they keep up the cycle of revolving debt, postponing taking care of the stuff that seems so far off. (Perhaps the first 15 seconds of this classic Queen song will help explain.)

So here’s the thing. In order to get on track and really start to feel like you’re making the better income level you’ve achieved, you need to spend a couple of years living like you’re making less to pay off that debt. It’ll be tough, but it’s doable. The blogosphere is packed with people who paid off tens of thousands of dollars in debt and they can’t wait to tell you about it. I’ll save you the reading and break it down into these three non-negotiables:

Non-negotiable #1: GET THE MATCH. If your employer has a 401(k) match, you should save at least enough to capture the match even if you could potentially lose it if you leave the company before it vests. Worst case scenario: you leave the job and lose the match, but you still get to keep the money you saved for retirement. Future you thanks you profusely and compound interest is excited to get to work for you.

Non-negotiable #2: STOP USING CREDIT CARDS UNTIL THEY’RE PAID OFF. I’ve seen too many people try to juggle paying off the new charges while also paying down balances and end up getting deeper and deeper in debt until they had to enter a formal debt management plan to get out of it. This could mean a few months of pain while you adjust to only spending the cash you have on hand, but it’s the only way you’ll see the light at the end of the tunnel. Make your credit card payment a fixed amount, then use the Debt Blaster calculator to pay it off. Once the debt is gone, you’ll already be used to not spending that amount of money, so you can use it to turbo-charge other savings goals.

Non-negotiable #3: GET A LITTLE NEST EGG SET ASIDE. There are personal finance celebrities who would say differently, but you need to have some savings set aside while you pay off debt or you risk sliding right back down the next time something unexpected pops up. When I started digging out of my debt hole in my 20’s, I also started saving $25 per paycheck into a separate savings account. I used that money if my only alternative was credit cards (read: a real emergency like having to buy a plane ticket for your grandma’s funeral, not a sale on your favorite Lulu® pants).

It won’t be easy, but it will be worth it. And keep these Jedi money mind tricks in mind to keep you from straying from the plan.

How To Tackle Tax Season

February 05, 2025

When the tax deadline approaches, it can be stressful, especially if

you are unsure if you have to pay the IRS. It’s too easy to procrastinate with

that potential IOU looming over your head. However, having a game plan to

organize and execute filing your taxes can take the bite out of tax season.

Gathering information

Build a tax file for your incoming tax statements. Getting it all

together saves the hassle of stopping in the middle of your tax preparation. Visit

your checking, savings, and online brokerage accounts for 1099s. Check your

mortgage provider for statements on interest paid. If you have an escrow, this may

also include property taxes. If not, check your local jurisdiction online to

download a statement.

One way to “de-stress” your tax planning is to know in

advance if you and the IRS agree on the facts of the previous year. Nothing is

more annoying than preparing your return and then getting that letter from the

IRS that they found a discrepancy. It can slow down the process of your tax

refund. You can view your official transcript with the IRS online account by

visiting Your

Online Account | Internal Revenue Service (irs.gov). (The IRS

made this easier by removing the biometric

data requirement.)

Getting your tax filing done

One recent survey shows that almost half (45%) of its respondents use tax planning software. Others (38%) choose to hire a tax preparer in person or virtually. The remainder prepares it the old-fashioned way. People with simple situations (no businesses, no real estate investment, and little to no investment income) are generally satisfied using tax filing software. However, one thing that can get overlooked is the options available to prepare your taxes for free if you fall below a certain income threshold. In addition, over 94% of individual tax returns are filed electronically.

Choosing a tax preparation method has much to do with your personal preference. For example, if you prefer to have a person prepare your return for you and your situation is relatively simple, a national chain franchise like H&R Block, Jackson Hewitt, or their local equivalent could be your cheapest and quickest solution. Just be aware that there is a wide variation in skills and experience among the people who work in these companies.

If your situation is complex or you have lingering issues

with the IRS, you may want to consider an Enrolled Agent or CPA specializing in

individual taxes. Enrolled Agents are authorized to represent you in front of

the IRS and earn their status either through experience as a former IRS

employee or by passing a 3-part comprehensive IRS test on individual and

business tax returns. You can search for a local one here. Like Enrolled Agents, CPAs can

represent you in front of the IRS and have even more rigorous requirements, but

they’re not necessarily more qualified as tax preparers. You will want to

interview your prospective CPA to determine how much of their practice they

dedicate to helping someone with the same tax concerns as you.

Plan for next year today

To make next year’s filing even less stressful than this year, begin planning before the year is over. Maintain that tax file for important documents as they come in throughout the year, so you do not have to pull it all together this time next year. If your refund is getting dangerously close to you having to pay, update your Form W-4 now to increase your withholding. Also, determine if putting more aside into your 401(k) or HSA could benefit you in the future.

Employer Retirement Plan Backdoor Roth Conversions

February 02, 2025

One increasingly popular strategy we have seen is the backdoor Roth conversion through an employer’s workplace retirement plan. If your employer’s plan allows, this strategy will enable you to convert after-tax voluntary 401(k) contributions to a Roth 401(k). When is it a good idea to contribute to an after-tax voluntary 401(k) and convert to a Roth 401(k)? Here are some factors to evaluate if you are considering this strategy:

Your plan allows after-tax voluntary contributions, and you want to save more than the pre-tax/Roth 401(k) 2025 elective deferral contribution limit of $23,500 or $31,000 if you’re over 50 years old.

You have a fully-funded emergency savings account, a reasonable debt situation, and do not need the liquidity.

You make too much to contribute to a Roth IRA but still want to save Roth dollars for your retirement.

You don’t want the hefty tax bill of a taxable conversion of pre-tax to Roth.

And most importantly, you love TAX-FREE money for your retirement!

The Basics

At a fundamental level, converting after-tax voluntary 401(k) money to a Roth 401(k) allows employees to save significantly more, tax-free, for retirement.

You don’t get a current-year tax deduction for the money deposited after-tax and then converted to a Roth 401(k), but the funds grow and are distributed tax-free as long as you hold the account until the age of 59.5 and it has been 5 years since your initial contribution into the Roth 401(k).

After-tax Voluntary Contributions in Work Retirement Plans

Some employer retirement plans allow employees to make three types of contributions 1) pre-tax, 2) Roth, and 3) after-tax voluntary. After-tax voluntary contributions have already been subject to income tax.

Generally, employees can contribute up to $23,500 (plus a $7,500 catch-up contribution if over 50, or $11,250 if age 60 – 63) to their pre-tax and/or Roth portion of the 401(k) in 2025. The combined annual IRS contribution limit is $70,000 in 2025 for most employer-sponsored retirement plans. Further, if your plan allows it and depending on whether your employer contributes or not, you may be able to make after-tax voluntary contributions above the basic limit.

It’s a good idea to work with your retirement plan administrator to find out exactly how much you can contribute (if the plan allows) to the after-tax voluntary account, but to get an idea, use the following equation:

After-tax Contribution Equation

$70,000 is the IRS limit in 2025

Minus

Pre-tax and/or Roth Contribution $23,500 (+$7,500 if over 50 years)

In addition to contributing to the after-tax voluntary portion of your 401(k), your company’s plan may allow you to convert this contribution to your Roth 401(k). You may be able to contribute up to $46,500 in 2025 of after-tax voluntary dollars and then convert all of it to your Roth 401(k)! That’s right – up to $46,500 growing tax-free for retirement. Some plans also allow you to roll this money outside the plan via a rollover to a Roth IRA.

What if my 401(k) Doesn’t Allow an In Plan Conversion?

If your plan doesn’t allow the backdoor option while working, you’ll have to wait until you separate from your employment. Typically, you can then roll after-tax voluntary contributions to a Roth IRA and after-tax voluntary earnings to a pre-tax Traditional IRA account, or you can convert the earnings and pay tax on that portion of the conversion.

Example

Henry has a great job as a software engineer. He earns a significant income and lives a simple life. He maxes out his pre-tax contribution to his 401(k), which is $23,500 in 2025, and his company contributes $9,500. Henry also contributes an additional $37,000 to the after-tax voluntary portion of his 401(k).

After-tax Contribution Equation Example

$70,000 is the IRS limit in 2025

Minus

Pre-tax and/or Roth Contribution $23,500 (+$7,500 if over 50 years)

His retirement plan allows him to convert the after-tax voluntary contributions to his Roth 401(k). In fact, if his plan allows, Henry can set up his conversions to happen automatically as soon as he contributes his after-tax voluntary dollars. He continues to convert the money to his Roth 401(k), building up tax-free funds for retirement.

Conclusion

The 401(k) Backdoor Roth Conversion is an excellent opportunity to save more for retirement in your 401(k) than the pre-tax and Roth contribution limits will allow. It makes the most sense for those who already have a stable financial foundation and do not anticipate liquidity needs before retirement.

Notes

* There are always exceptions to the rules, so before conversion, seek advice from a tax expert that will help you understand the conversion’s tax implications to your specific situation.

* There may be plan-specific rules. Please check with the administrator for your workplace retirement plan.

* There are different distribution rules for after-tax voluntary contributions made before 1987. Consult your tax advisor for more information.

* Conversions may affect net unrealized appreciation (NUA) treatment on employers’ stock positions.

How To Save For Retirement Beyond The 401(k)

February 02, 2025

Preparing for retirement is an essential part of financial planning. Employer-sponsored retirement plans, such as 401(k) plans, are a common tool for saving. While contributing to a 401(k) can be a great way to save for retirement, it’s important to consider other options as well.

First things first

Are you fortunate enough to work for a company that offers to match employer-sponsored retirement plan contributions? If so, you should put the required minimum into the account to get that free money. Doing less is basically like turning down a raise!

Once you’re doing that, there are reasons that you may want to save additional funds outside the 401(k). Of course, if you don’t have a match or a 401(k) available, you may also need another way to save. Besides not having a 401(k) option, the most common reason to invest outside a 401(k) is investment selection. So, here are some other common options:

IRA

For the self-employed, there are actually many different tax-advantaged retirement accounts you can contribute to. If you work for a company that doesn’t offer a retirement plan, you can still contribute to an IRA. If this is the case, you can contribute up to $7,000 (or $8,000 if 50+) to an IRA. Additionally, you can deduct traditional IRA contributions no matter your income. However, income limitations exist on deducting contributions when you already have a 401(k) or 403(b) available.

A popular choice these days is the Roth IRA. This is partially because of the tax benefits. However, there is also more flexibility in accessing Roth IRA money early versus traditional or even Roth 401(k)s. For example, you can withdraw your Roth IRA contributions without taxes or penalties. Another benefit is your ability to withdraw up to $10k in growth for a first-time home purchase. You don’t have that option with a 401(k), at least not without tax consequences.

HSA

If you have access to a high-deductible health insurance plan, you can contribute to a health savings account (HSA). Contributions are limited to $4,300 per person or $8,550 per family (plus an extra $1,000 if age 55+). The contributions are tax-deductible, and the money can be used tax-free for qualified health care expenses. If you use the money for non-medical expenses, it’s subject to taxes plus a 20% penalty. However, the penalty goes away once you reach age 65, turning it into a tax-deferred retirement account that’s still tax-free for health care expenses (including most Medicare and qualified long-term care insurance premiums). You may also consider avoiding using the HSA even for medical expenses and investing it to grow for retirement.

US Government Savings Bonds

Each person can purchase up to $10k per year in Series EE US Government Savings Bonds. For Series I Savings Bonds, that limit is also $10k. The federal government guarantees these tax-deferred bonds, which don’t fluctuate in value. As such, they can be good conservative options for retirement savings. However, you can’t cash them in the first 12 months, and you lose the last 3 months of interest if you cash them in the first 5 years. Interest rates may remain low, but the I Bonds are based on inflation, which is slowly creeping up.

Regular account

If you’ve maxed out your other options, you can always invest for retirement in a regular taxable account. You can minimize taxes by investing according to your tax bracket. For example, invest in tax-free municipal bonds if you’re in a high tax bracket. Holding individual securities for at least a year will keep capital gains taxes low. You can also choose low-turnover funds like index funds and ETFs. Another strategy is to use losses to offset other taxes, including up to $3k per year from regular income taxes. The excess carries forward indefinitely. Just be aware that if you repurchase an identical investment within 30 days, you won’t be able to take the loss off your taxes.

Regardless of how you choose to save for retirement, the most important thing is that you save enough. Run a retirement calculator to see how much you need to save. Then, increase contributions through payroll or direct deposit. If you can’t save enough now, try gradually increasing your savings rate each year. Like it or not, your ability to retire depends on you.

Rolling Voluntary 401(k) After-Tax Money To Roth IRA

February 02, 2025

Using after-tax 401(k) contributions to execute backdoor conversions to a Roth IRA can be an effective strategy if you want to utilize these funds to retire early. When do employees think about executing this strategy? Consider the following factors:

You want to retire early

A large portion of your net worth is tied up in retirement accounts

Your work retirement plan allows for after-tax contributions to your 401(k) into a separate account

Your plan also allows in-service direct rollovers from the after-tax account to a retirement account outside of the plan

You have (or will have) savings or investments in outside retirement accounts that can help to supplement your early retirement

The Basics

At a fundamental level, after-tax Roth IRA conversions allow folks who retire early access to retirement principal without the 10% penalty typically assessed on early withdrawals from these accounts.

In a Roth IRA, you can access contributions anytime because you have already paid tax on the money. You can access the after-tax conversion basis directly rolled into your Roth IRA from your 401(k) without penalty as well. However, each taxable conversion has its own 5-year rule, and if you withdraw the funds within the first five years, unless you have a qualifying reason, the withdrawal may be penalized.

Investments in Roth IRAs have the potential to grow with the market, and earnings are distributed tax-free as long as you hold the account until the age of 59.5 or 5 years, whichever is longer. You may be able to withdraw from your Roth IRA if you have a qualifying reason to take the money out.

Seek tax advice before any conversion so you understand the tax implications for your specific situation.

After-tax Contributions to Work Retirement Plans

Certain employer retirement plans allow employees to make three types of contributions:

Pre-tax/regular

Roth

After-tax voluntary

Employees can contribute up to $23,500 (plus a $7,500 catch-up contribution if over 50 years of age, or $11,250 if age 60 – 63) to the pre-tax and/or Roth 401(k) portion of the retirement plan in 2025.

In addition, if your plan allows it and depending on if your employer contributes or not, you may be able to contribute up to another $46,500 to the after-tax voluntary bucket. The IRS aggregate limit of employer and employee contribution increased to $70,000 in 2025 for most workplace retirement plan accounts like 401(k)s.

Use the following equation to figure out how much you can contribute to the after-tax bucket in your retirement plan through work:

After-tax Contribution Equation

$70,000 is the IRS limit in 2025

Minus

Pre-tax and/or Roth Contribution$23,500 (+$7,500 if over 50 years)

In-Service After-tax Voluntary Conversion to a Roth IRA

Generally, when completing a 401(k) after-tax voluntary conversion to a Roth IRA, the conversion principal from a direct after-tax rollover is deposited into a Roth IRA, and earnings are rolled over into a Traditional IRA. However, earnings can also be converted to a Roth and tax paid.

When money is converted from the after-tax voluntary bucket of a 401(k) to a Roth IRA over a series of years, employees can build a significant amount of converted principal available to be accessed in early retirement that would otherwise likely be locked up until age 59.5. Though the conversion basis can be accessed, if conversion earnings are distributed before 59.5 and/or five years, whichever is longer, the gains are taxed and penalized.

Why can’t I access these converted funds in my Roth 401(k)? *

In most cases, pre-retirement pro-rata distribution rules apply to unqualified early distributions from a 401(k). If you have a Roth 401(k) and take an early distribution, it will most likely be a mix of taxable (with penalty) and nontaxable funds.

How and when can I access money from a Roth IRA without penalty?

Always access your contributions penalty-free

Taxable conversions are penalty-free five years after the conversion

You can access the nontaxable conversion principal penalty-free at any time

Access earnings free and clear after 59.5 or five years, whichever is longer

Let’s say you are 30 years old and looking to retire before the age of 50. Having money in a retirement account that is accessible, without penalty, is important regardless of age. Each year for 10 years, you make after-tax contributions to your 401(k) of $10,000, which grow to $11,000 before you request an in-service conversion rollover of this money into a Roth IRA. You invest the Roth IRA for growth, and it earns another $10,000. That growth will be tax and penalty-free as long as you wait until age 59.5 and at least five years to withdraw the earnings. However, the basis that you have converted over the years from your after-tax voluntary 401(k) account can be taken out without penalty or tax, regardless of age.

Here is what happens if you decide to withdraw the entire amount prior to age 59.5:

401(k) Contributions and Gains After-tax contributions to 401(k) – $100,000 Total gains realized on after-tax contributions – $10,000

Backdoor Conversion to Roth IRA Basis converted to Roth IRA – $100,000 Growth converted to Roth IRA and taxed upon conversion – $10,000

Withdrawal from Roth IRA prior to age 59.5 Contributions (tax and penalty-free) – $0 Taxable Conversion (10% penalty if held less than 5 years) – $10,000 After-Tax Conversion (tax and penalty free) – $100,000 Gains realized after conversion to Roth IRA (taxable and 10% penalty) – $10,000

Important Notes

* There may be plan-specific rules. Please check with the administrator for your work retirement.

* There are always exceptions to the rules, so before conversion, please seek advice from a tax expert that will help you understand the conversion tax implications.

* There are different distribution rules for after-tax contributions made before 1987. Consult your tax advisor for more information.

* Conversions may affect net unrealized appreciation (NUA) treatment on employer’s stock positions.

7 Ways to Start Earning More Money Today

January 21, 2025

What do you think of when you hear the word “budget”? Chances are, it makes you think of restrictive things like sacrificing or cutting back. But a budget is simply a tool to help us achieve our life goals more deliberately and successfully. One way to balance a budget is to cut back, but another way is to increase income. Here are seven ways to do that – several of which I’ve done myself.

1. Become a Tasker on TaskRabbit. Have you learned how to read the language of IKEA assembly directions, or do you get a special thrill from the sound of the vacuum sucking up debris? These are just two everyday skills people are willing to pay someone else to do. Take a look at their website to see what skills of your own you may be able to put to use.

2. Childcare. Overworked parents will pay a teenager top dollar to watch their kids for a night out. Imagine what they’d pay a fully employed, responsible adult…easy money! Even services like Care, Sittercity, and Babysitease connect you with families seeking help. I was a sitter for BabysitEase in Cincinnati, and it was great! If I had a Saturday night with no plans, I just logged into the website and signed up for whichever family looked like the most fun for me.

3. Pet-sit. If kids aren’t your thing, consider offering your services as a pet sitter. This idea is another side gig I held until recently. I signed up for a local pet-sitting franchise that performed a background check on me and then offered to check in on people’s cats and dogs while they were out of town. I only did the ones I wanted to, and they did all the work of collecting the money, providing insurance in case something happened, etc.

4. Teach others your hobby. Are you the person your friends and family turn to with questions about technology, fitness, or even just how to apply their makeup properly? Services like Dabble are a great way to teach others how to do what you love while making some extra cash. I have an acquaintance who uses Dabble to teach other crafters how to knit and crochet on weekend afternoons.

5. Sell the products of your hobby. Several years ago, I signed up for a booth at a local craft fair where I sold fingerless hand-warmers that I had knitted myself while binge-watching the latest show. One of my ongoing coaching clients uses Etsy to sell her original paintings to escape her paycheck-to-paycheck lifestyle without leaving her beloved apartment. It doesn’t cost anything to set up your store.

6. Personal shopper. Everyone knows their way around the grocery store or can easily learn to navigate one. A friend recently told me how she easily started shopping with Instacart to earn some extra cash when her hours at work decreased. She mentioned how user-friendly the app was and how friendly the people she’d delivered to were, often giving a nice cash tip after dropping off the groceries.

7. Charge for your carpool. I’ve met some of the most interesting people while riding around town in rideshare cars via Uber and Lyft. They are authors, nurses, and even office workers who give one ride each day after work before heading home.

No matter what way you decide to earn some extra cash, make sure you take the extra step and apply that cash toward your savings goals. While the money you earn may seem like just a little, it adds up. Make the most of your spare time to help get you where you want to go faster.

Insider Tips: How To Work with Your Creditor to Adjust Payment Terms

January 21, 2025