How To Invest For Income In Retirement

October 26, 2018

All your working life you’ve been saving and investing some of your income for retirement. Now you are getting ready to leave full time work and begin to spend it. How do you figure out how to invest so that your money lasts for what is hopefully a long and happy life? Whether you are a DIY investor or working with an advisor, consider these general guidelines for investing to generate retirement income:

Create both fixed and flexible sources of income

Right now, you have investments that you own. If you are like many retirees, it may make you nervous to spend your assets. Income, on the other hand, is psychologically easier to spend. Rather than spending them down, think about how you can invest some of your assets to create income.

One possible goal of retirement income planning is to create both fixed and flexible income. Fixed income is income you can rely on to arrive at predictable times and in predictable amounts. Social Security is fixed, for example. Ideally, you would create enough fixed income to cover all your fixed, must-pay monthly expenses like housing, transportation and food.

Ways to create fixed income besides Social Security

Pension annuity: Most pension plans have distribution options that include several level monthly payment options as well as a lump sum distribution. Choosing the annuity will offer you level monthly payments, which you cannot outlive in most cases. Married couples can choose a “joint and survivor” option, which makes monthly payments until the death of the second spouse. Not sure if it makes sense to take the monthly annuity or the lump sum? See this blog post for guidance.

Create your own pension by buying an annuity: The traditional pension is an endangered species, so if you don’t have one, you can create your own personal “pension” by purchasing an immediate annuity with some of your retirement savings. Per ImmediateAnnuity.com, a 65-year old man in North Carolina would receive $527/month in exchange for $100,000. This turns your lump sum into a monthly income stream.

Immediate annuities vary from insurance company to insurance company, so run the numbers and do your research before you sign on the dotted line. Remember, you’re looking for consistent monthly income that covers just your fixed expenses. Don’t use all your assets to purchase an annuity. Otherwise you may not leave yourself enough flexibility to meet variable expenses like vacations and entertainment, or unexpected larger expenses like a dental emergency, a new car or a new furnace. Click here to learn more about the ABCs of annuities and here for some situations where they might make sense.

Bonds: A bond is a fixed income investment where the investor is essentially loaning money to a corporation or government entity for a fixed period of time at a fixed or variable rate of interest. There are many types of bonds, with different features and different levels of investment risk. You can invest in them directly or through bond mutual funds, closed end funds or exchange traded funds.

Bond interest is often paid semi-annually, so retirement income investors typically look for a diverse portfolio of bonds so there is some interest coming in every month. The base of a diversified bond portfolio should be “investment grade” bonds, which are issued by companies with a high credit quality, and U.S. Treasury securities, which are bonds issued by the U.S. government. Click here to learn more about how bonds work and how to build a bond ladder.

Dividend-paying stocks: Dividends are a share of company profits paid out regularly to shareholders. High quality, dividend-paying stocks can provide quarterly income, as well as the potential for appreciation. Like bonds, there are several types of dividend-paying stocks, with different features and different levels of investment risk. Dividends from preferred stock (which generally don’t have voting rights) tend to be higher than dividends from common stock.

You can invest in dividend-paying stocks directly or through stock mutual funds, closed end funds or exchange traded funds that focus on dividends. Funds in this category are usually described as “dividend income,” “dividend,” or “preferred stock” funds. Make sure to do your research and read the prospectus before investing.

If you hold dividend-paying stocks in a taxable brokerage account, look for shares which pay “qualified dividends.” Those are taxed at lower long-term capital gains tax rates of 0 to 20 percent, depending on your total income. Learn more about dividend-paying stocks here.

Real Estate Investment Trusts: A Real Estate Investment Trust (REIT) is a company which owns or finances income-producing real estate. Most REITs are publicly traded on major stock exchanges, but some are private. By law, REITs must pay out 90% of their taxable income in dividends annually. REIT dividends are usually taxed as ordinary income. You can invest in publicly traded REITs individually and through closed end funds, exchange traded funds and mutual funds.

While REITs hold portfolios of rental real estate or mortgages, remember that they have many of the same risks as investing in stocks. Generally, it’s a good idea to limit your REIT exposure to 5 to 10 percent of your portfolio, and just like stocks, REITs aren’t a fit for every investor. Adding real estate to a diversified portfolio of stocks and bonds can usually reduce portfolio volatility though.

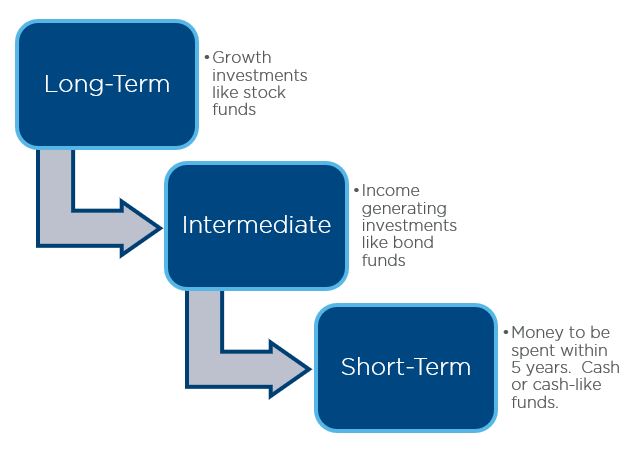

Maintain purchasing power over the long term

Inflation has been low for the past two decades, but it hasn’t always been that way. Remember the interest rates on passbook savings accounts in the seventies? When you were working, you could rely on your salary increasing (at least somewhat) to keep pace with inflation.

In retirement, if you don’t include investments that generally move up when inflation does, you’ll be losing purchasing power. Click here to read more about protecting your portfolio from the effects of inflation. Investments that can help your portfolio from the inevitable rising cost of living include:

Stocks: A well-diversified portfolio of individual stocks, stock mutual funds or exchange traded funds that grows in value over time can offer a hedge or partial hedge against inflation. Some of the hedging effects come from dividends and some from growth. Wharton School professor Jeremy Siegel suggests that to best insulate a portfolio against inflation, it is necessary to invest internationally. For many retirees, some growth will be required to maintain purchasing power given that a typical retirement could last twenty to forty years.

Treasury-inflation protected securities: TIPS are treasury bonds that are indexed to inflation. The interest rate remains fixed, and the principal increases with inflation and decreases with deflation. It’s best to hold TIPS in a retirement account to protect against paying taxes on phantom income if the bonds adjust upwards.

Inflation adjusted annuities: If you have chosen to purchase an annuity, consider purchasing one where the payment is indexed to inflation. Like a traditional annuity, an inflation-protected annuity pays you income for the rest of your life, but unlike a traditional annuity, the payment rises if inflation rises. Consequently, the initial payout is likely to be lower than with a traditional annuity.

Rental real estate: Real estate tends to perform well with rising inflation. Rental income generally keeps pace with inflation, and inflation can increase the value of your property. However, being a landlord is not for everyone, and it’s difficult to get a diversified rental income portfolio without a large investment. Direct real estate investing has both advantages and challenges. If you are considering rental real estate, take this quiz first.

Prepare for longevity

According to the Social Security Administration, the average 65 year old man today is expected to live until age 84.3, and the average 65 year old woman until age 86.6. Since these are averages, that means some of these 65 year olds will live longer. That’s going to cost some money.

A longevity annuity is a new financial product that helps protect you against the risk of outliving your money. It typically requires you to wait until very late in retirement to begin receiving payment – e.g., age 85 or later. Once the payout period begins, it offers income for the rest of your life. The IRS permits the purchase of longevity annuities within retirement accounts, subject to certain limitations, and they are excluded from the calculation of required minimum distributions (RMDs).

A version of this post was originally published on Forbes