What Are Your Health Insurance Options When Retiring Early?

February 20, 2017

Are you considering retiring before age 65 but worried you could lose your access to health insurance due to the new administration’s promise to repeal the Affordable Care Act? There’s a lot up in the air right now, and it’s going to take some time to play out in Congress. Health insurance is expensive, and health care costs are likely to comprise a large chunk of your retirement spending.

Up until now, if you are like most Americans, you have participated in a group health plan with your employer subsidizing the cost. With family coverage, the typical full cost of coverage is over $18,000 per year. If you retire early, you’ll need to find and pay for new health care coverage until you are age 65 and can participate in Medicare. Here are some strategies for making wise decisions in the face of increasing uncertainty about health insurance access and costs.

Don’t Panic

It may feel like the earth is being demolished to make room for an intergalactic freeway, but don’t panic. The health insurance landscape could look a lot different next year than it does now – or it may not. We don’t know very much for sure except that there is uncertainty.

Under those circumstances, it’s helpful to plan for multiple scenarios: health insurance costs more and/or is harder to obtain, waiting periods for pre-existing conditions could be reinstated, or the major provisions of the ACA are not repealed. Prepare an early retirement budget which reflects your projected health insurance costs under each of these scenarios. Remember – you only need to model the changes through age 65, when Medicare kicks in.

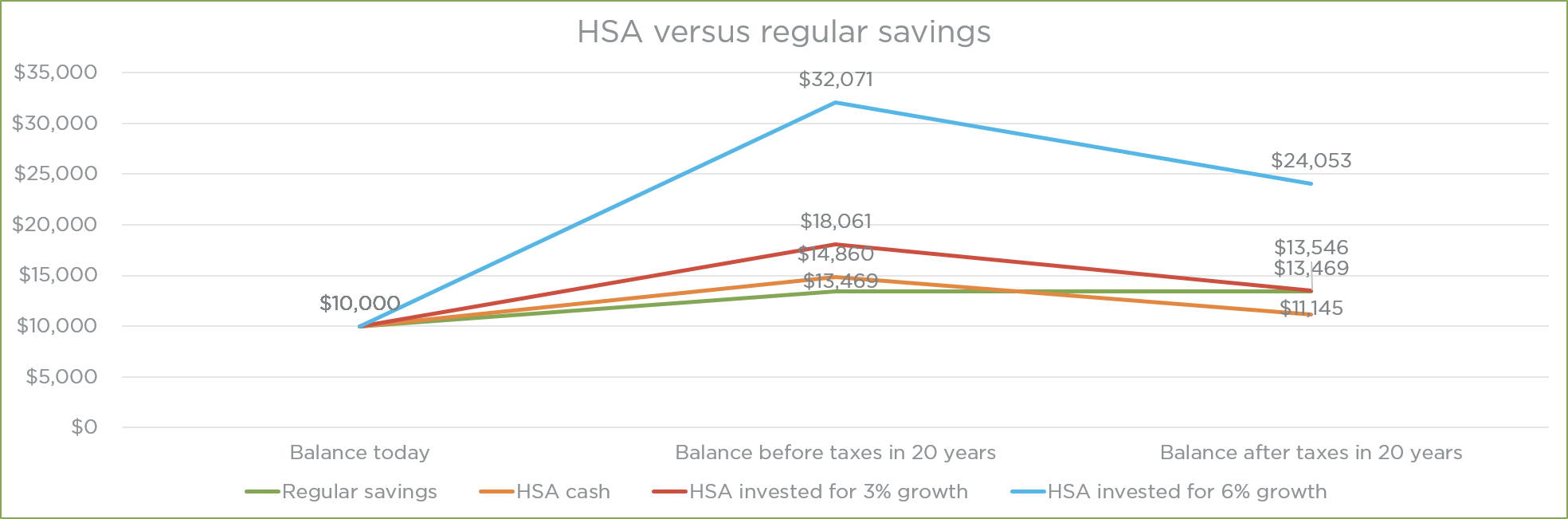

Build up your HSA – and don’t spend it

If you are currently covered by a high deductible health plan (HDHP) with a health savings account (HSA), build up your balance as much as you can. Contribute the maximum to your HSA between now and your retirement date. Those with individual coverage can contribute a maximum of $3,400 and those with family coverage can contribute a maximum of $6,750 for 2017. If you are 55 or older, you may contribute an additional $1,000.

Once you’ve contributed those funds, if possible – don’t spend them. Use other available cash reserves to pay for your routine expenses up to the deductible. After you have built a balance greater than your out-of-pocket maximum for the year, consider investing the remainder.

For those retiring early, keep as much of your HSA balance as possible to pay for eligible medical expenses after you retire, including COBRA premiums (see below) as an early retiree and Medicare Parts B, D and Medicare Advantage after age 65. For IRS guidelines on HSAs see here. For more ideas on maximizing your HSA see here.

Increase your cash reserves

The years leading up to an early retirement are a great time to power up your cash reserves. Work towards building short term liquid savings such as a savings account, money market fund, short duration CDs or Treasury Bills equal to several years’ worth of projected maximum out-of-pocket health care costs.

Look for part-time work with access to health care benefits

Many early retirees have discovered that the key to managing health care costs in retirement is to work part-time. Ask yourself if it makes sense to look for part-time work through age 65, either with your existing company or another, such as these companies who offer insurance coverage to their part-time employees. You will probably have to cover all or most of the cost of your health insurance. However, participation in a group plan may offer more comprehensive coverage. It also isn’t going to hurt to have some extra money coming in the door during the early retirement years to help pay health care costs.

Consider COBRA

When you retire, you may continue your group coverage under COBRA for 18 months, paying the full premium yourself (or with retiree health plan dollars if you are fortunate enough to have a retiree health plan). As mentioned above, if you have funds in your health savings account (HSA), you can use them to pay for insurance premiums for health care continuation coverage through COBRA. Your coverage continues during the same period, and you won’t have to change providers or get used to a new procedure for submitting claims. Be aware: there will be some sticker shock as you begin to pay the entire cost of your health insurance premium.

If you have a pre-existing condition and are retiring within 18 months of when you’ll be 65, COBRA is likely to be your best option in this age of uncertainty. As long as you pay your premiums, you’ll remain covered up until you’re eligible for Medicare. Even if you don’t have a pre-existing condition, choosing COBRA still gives you a little breathing room to figure out your next steps for insurance once it’s clear what happens to the ACA.

Price coverage on the private market

If you are in good health, consider pricing your options in the private insurance marketplace. The younger your early retirement begins, the more it could make sense to shop around for the right insurance. The private market offers a wider range of options. Compare plans and prices by using online marketplaces such as ehealthinsurance.com or gohealthinsurance.com or working directly with an insurance broker. Even if you are considering coverage under COBRA or the Affordable Care Act, it’s a good idea to shop around and compare.

Take your chances now with the ACA

The Affordable Care Act is still the current law and the infrastructure which allows consumers to buy insurance is still firmly in place. If you are planning to retire soon, you may consider applying for coverage under the ACA and comparing plans to COBRA and what you found through the private market. Even if you retire outside of the open enrollment period, losing your employer-provided coverage is a qualifying event. Start at Healthcare.gov to see what is available in your state.

Depending on your new family income after early retirement, you may qualify for a subsidy of your insurance premiums. However, that is something which could change quickly, so it’s best not to count on it. In any case, you cannot be turned down for coverage. There are many advantages to the ACA for early retirees if the law remains the same or amended: cost savings, universal access, subsidies for lower income participants, etc. The biggest disadvantage right now for early retirees in buying insurance is not knowing whether the same or similar coverage will be available if the law is repealed.

In conclusion, for those considering early retirement, the uncertainty about what’s going to happen to the Affordable Care Act has added a layer of complexity to pre-retirement preparations. For some employees, they may decide it’s best to delay their planned early retirements until there is more clarity about what happens next. For others, they may choose to forge ahead, hopefully with bigger balances in their HSAs and savings accounts to help manage the risk that comes along with this uncertainty. If you have strong opinions about the ACA and what Congress and the President should do next, you can find information about how to contact them here.

Do you have a question you’d like answered in this column? Please email me at [email protected]. You can follow me on our Financial Finesse blog by signing up here, and on Twitter@cynthiameyer_FF.